Operational Drag: Associates spent hours each week on follow-up and error correction.

Compliance Exposure: The lack of a unified process led to a high rate of missing signatures and document errors, delaying account activation for clients.

Client Relationship Risk: The inefficient and opaque process frustrated both associates and their clients, straining trust from RBC.

The core challenge was architectural, not aesthetic.

Success depended on designing a new information and workflow architecture that could handle the complexity of financial households.

Rationale: This prioritized reduced cognitive load and ensured compliance which is a non-negotiable in wealth management.

Validation: This trade-off was proven correct in testing, where users explicitly preferred the guided approach over the burden of configuration.

Action: Instead of dismissing it, I collaborated with the Product Manager to classify "Download Draft" as a post-MVP feature.

Result: This demonstrated strategic product thinking, ensuring we launched a focused, core experience while designing a scalable solution that could be integrated later.

With our architectural decisions defined, the goal was to translate them into a high fidelity, interactive prototype.

This artifact was purpose built to validate our core hypotheses around the unified household view and streamlined signer management.

I prioritized high-fidelity prototyping over extensive low-fi wireframing to provide stakeholders and users with a realistic experience of the proposed workflow.

This allowed for more meaningful feedback on the core concepts of household management and the proposed IA.

The prototype was designed to test three key hypotheses:

1. Could associates manage all household documents from a single page?

2. Was the process for adding signers clear and efficient?

3. Did the review and send flow feel cohesive and error proof?

United Document Management Page: The central hub consolidating all account and client documents for the entire household.

Additional Signers Flow: The streamlined process for managing beneficiaries and co-signers within the main workflow.

Review & Send Experience: The final validation step allowing associates to confirm the complete package before sending.

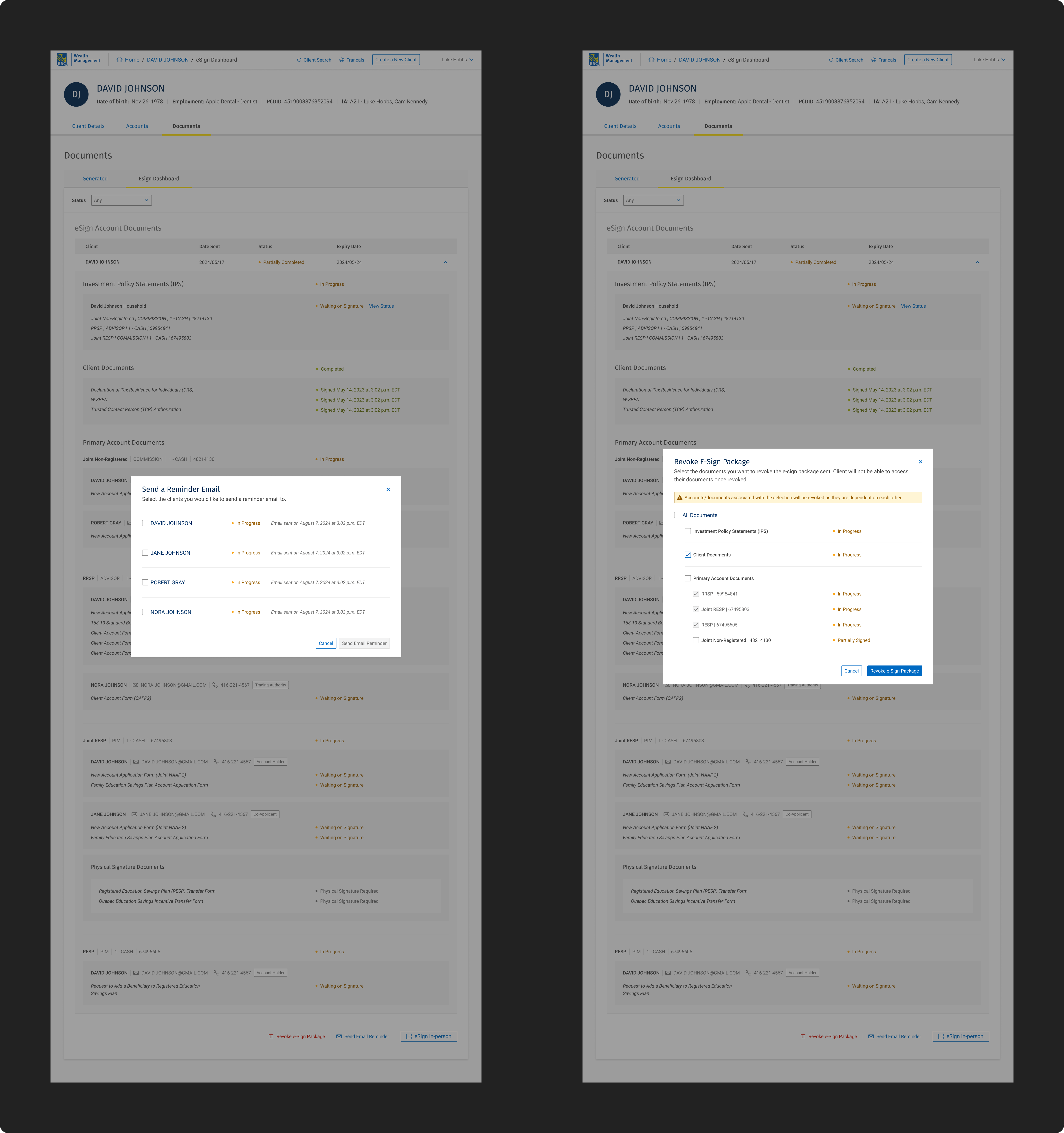

eSign Dashboard: The post send status tracker for monitoring signature completion.

The Validation: Proving the Core Concept

100% Task Completion Rate: All users successfully navigated the entire consolidated household flow, providing undeniable validation for the new architectural model.

High User Satisfaction (Avg. 4.6/5): The unified system was praised for its intuitiveness and potential to save time. One associate noted, “This is revolutionary.”

Signer Management Microcopy: 3 of 5 users struggled with the language in modals and CTAs, indicating a need for clearer, more contextual messaging.

Navigation & Context: Users desired documents expanded by default for a better overview and clearer status indicators on greyed out items.

The "Download Draft" Request: Emerged as a strong user need for offline verification, a feature we had deliberately scoped out of the MVP.

Quick Wins (High Impact, Low Effort): Fix confusing product copy on modals, set documents to expanded view by default, update notification types from 'warning' to 'info'.

Major Initiatives (High Impact, High Effort): Develop the "Download Draft" functionality, redesign the post send dashboard navigation to a consolidated household view.

Low Priority (Low Impact): Minor visual tweaks and copy changes.

The finalized high-fidelity prototypes incorporated the prioritized "Quick Win" refinements and embodied the core architectural decisions.

Each screen was designed to validate our initial hypotheses and resolve the key pain points of the original workflow.

Hypothesis Validated: A single page system reduces errors and improves efficiency.

Design Rationale: This hub consolidates all client and account documents for the entire household. Based on testing feedback, documents are expanded by default to provide immediate visibility and context, eliminating the need for manual discovery.

Hypothesis Validated: Flexible signer management accommodates complex households.

Design Rationale: The process for adding beneficiaries and co-signers is integrated into the main flow via a clear modal, maintaining task continuity. Microcopy and CTA language were refined post testing to eliminate ambiguity.

Hypothesis Validated: A consolidated system reduces frustration and errors.

Design Rationale: This mandatory review step acts as a final "quality gate," providing a comprehensive overview of the entire household package.

Built-in validation logic ensures all required signatures are assigned before sending, directly preventing the errors that caused onboarding delays

Hypothesis Validated: A consolidated system reduces frustration and errors.

Design Rationale: This dashboard provides a transparent, real-time status tracker for every document and every member of the household.

The design balances familiarity with the existing system with the new need to view status by household, a key insight from testing.